Too Much Roth? Wondering after listening to Ep 583

I have listened to a bunch of episodes now of the choose fi podcast. I have been bouncing around episodes and I just landed on the Incremental Gains and the detour episode (582 & 583). I love them as rapid (ish) fire points, but the Detour episode had me scratching my head to some extent.

For Context: I am a firefighter and my wife has a more normal job. We are both 36 years old. I have been contributing to my 457 since I started my job ten years ago. These contributions have been all Roth, and total about 62,000. My wife has a 401k through her job that has a 3% employer match with a 6% employee contribution. She has contributed and has a total of about 80,000 in this account. A year or two she switched these contributions to Roth as well, so a small percentage of that account is Roth. We have approximately 26,500 combined in Traditional IRAs from old 401ks. We have approximately $3000 in Roth IRA as well. We currently have a mortgage with a balance of approximately 146,000 with an interest rate of 5.99. It is due to be paid off in November of 2042 (16 years). We had been paying aggressively on it but I think it will be more beneficial to put that money to work for us instead of just building equity. As it stands right now we are able to invest/save about 2,000 a month, As we optimize more, it will grow.

Anyway, my plan that I had hatched was to max out our Roth IRAs going forward and also to sock money into our taxable brokerage account. This, while continuing to get the match in my wife's 401k (switch back to traditional??) and also continue to contribute to my 457 (again change to Traditional or continue with Roth?)

We have a goal of buying a second property for recreation in about ten years. We have a one year old daughter and would love to have the property in the family when she is able to enjoy it. We are thinking either hunting land or a cabin on or near a lake. We also want to take our daughter on an Alaska cruise around that same time. With this 10 year goal, and 16+ years left to work, I don't want to just load up my 457, as I can't access this until I retire. I plan to finance these with Taxable Brokerage money, and possibly Roth IRA contributions if needed.

I am not truly looking to retire early, as I can retire with full pension at Age 53. I have calculated this (and also am most of the way through listening to "The Golden Albatross") to be about 7,000 a month that my pension will pay out, using conservative estimates of raises and overtime oppurtunities. This being said, it is also a goal that my wife could retire around the same age as me, where we thought in the past she would need to keep working.

All this being said, I am wondering if I should reconsider so much Roth and switch some contributions to traditional. I ran it through Chat GPT and it seems I could save about $1000 a year just by switching my Deferred Compensation (457) contributions to Traditional. My thought is that when my wife and I retire we will go from two incomes down to my pension income. This could perhaps have some opening for optimization with either drawing from my 457 at a reduced tax rate (if I switch to Traditional now) while still having large Roth options. These would include the money in our Roth IRAs and the growth on my 457 up to this point. Rule of 72, this would hopefully be around 240,000 at that point.

I would love to be a part of a case study if that would be an option. Maybe there are things I have not thought of in this as far as optimization. I have listened to the episodes with Grumpus Maximus and The Millionaire Educator. Loved the "Is my Pension Safe" episode and learned a lot from that. Any other episodes I should look at?

Thanks to anyone that reads through all of this.

I have listened to a bunch of episodes now of the choose fi podcast. I have been bouncing around episodes and I just landed on the Incremental Gains and the detour episode (582 & 583). I love them as rapid (ish) fire points, but the Detour episode had me scratching my head to some extent.

For Context: I am a firefighter and my wife has a more normal job. We are both 36 years old. I have been contributing to my 457 since I started my job ten years ago. These contributions have been all Roth, and total about 62,000. My wife has a 401k through her job that has a 3% employer match with a 6% employee contribution. She has contributed and has a total of about 80,000 in this account. A year or two she switched these contributions to Roth as well, so a small percentage of that account is Roth. We have approximately 26,500 combined in Traditional IRAs from old 401ks. We have approximately $3000 in Roth IRA as well. We currently have a mortgage with a balance of approximately 146,000 with an interest rate of 5.99. It is due to be paid off in November of 2042 (16 years). We had been paying aggressively on it but I think it will be more beneficial to put that money to work for us instead of just building equity. As it stands right now we are able to invest/save about 2,000 a month, As we optimize more, it will grow.

Anyway, my plan that I had hatched was to max out our Roth IRAs going forward and also to sock money into our taxable brokerage account. This, while continuing to get the match in my wife's 401k (switch back to traditional??) and also continue to contribute to my 457 (again change to Traditional or continue with Roth?)

We have a goal of buying a second property for recreation in about ten years. We have a one year old daughter and would love to have the property in the family when she is able to enjoy it. We are thinking either hunting land or a cabin on or near a lake. We also want to take our daughter on an Alaska cruise around that same time. With this 10 year goal, and 16+ years left to work, I don't want to just load up my 457, as I can't access this until I retire. I plan to finance these with Taxable Brokerage money, and possibly Roth IRA contributions if needed.

I am not truly looking to retire early, as I can retire with full pension at Age 53. I have calculated this (and also am most of the way through listening to "The Golden Albatross") to be about 7,000 a month that my pension will pay out, using conservative estimates of raises and overtime oppurtunities. This being said, it is also a goal that my wife could retire around the same age as me, where we thought in the past she would need to keep working.

All this being said, I am wondering if I should reconsider so much Roth and switch some contributions to traditional. I ran it through Chat GPT and it seems I could save about $1000 a year just by switching my Deferred Compensation (457) contributions to Traditional. My thought is that when my wife and I retire we will go from two incomes down to my pension income. This could perhaps have some opening for optimization with either drawing from my 457 at a reduced tax rate (if I switch to Traditional now) while still having large Roth options. These would include the money in our Roth IRAs and the growth on my 457 up to this point. Rule of 72, this would hopefully be around 240,000 at that point.

I would love to be a part of a case study if that would be an option. Maybe there are things I have not thought of in this as far as optimization. I have listened to the episodes with Grumpus Maximus and The Millionaire Educator. Loved the "Is my Pension Safe" episode and learned a lot from that. Any other episodes I should look at?

Thanks to anyone that reads through all of this.

Join the conversation

Sign up to reply, follow discussions, and connect with the ChooseFI community.

Comments

IMO if you're in the 22% tax bracket or above, it's better to contribute to Trad rather than Roth 401k. The reason is that for virtually all retirees, the amount they spend in retirement is less than they amount they earn during their work years, especially with kids moving out or a mortgage paid off. And if you're planning to withdraw some from taxable brokerage in retirement, then the cost basis portion of the withdrawals is not taxed, meaning your income will be even less. Traditional 401k gives you the optionality of doing conversions when you retire or are laid off, where as Roth 401k gives you no optionality.

The Roth vs. Traditional question comes down to tax arbitrage. As Roberto mentions, your $84K pension will put your top tax bracket at 12%, assuming tax brackets in 16+ years are similar to what they are now.

You don't mention what projected future annual spend may be, but with a young child and plans to buy property and travel, your spending may push you into the 22% bracket. So in a theoretical future, distributions out of your traditional accounts would be taxed at either 12% or 22% since the pension fills up the lower brackets. Compare that to what tax you're paying today on Roth workplace plan contributions to decide whether Roth or Traditional now saves on tax.

To help you think through these possibilities, I highly recommend picking up a copy of  Cody Garrett, CFP® and Sean Mullaney's book, Tax Planning To and Through Early Retirement. It's a great reference and I find I go back and reread sections as I'm thinking though tax planning.

Cody Garrett, CFP® and Sean Mullaney's book, Tax Planning To and Through Early Retirement. It's a great reference and I find I go back and reread sections as I'm thinking though tax planning.

Tax Planning To and Through Early Retirement - Book Details

I agree with your plan to no longer pay extra toward your 6% mortgage and instead direct those dollars toward investments. This is interest rate arbitrage as those dollars are likely to earn more than 6% invested in the market.

Thanks!

Be careful with those "on the fly" Chat GPT questions. GPT will answer them with confidence without actually doing the math. I think AI can be useful only to the extent you coach it through the calculations. Claude is better at building spreadsheets and showing you its work, but still usually has bugs in it for the first 5+ revisions. In your case, I think you would benefit from either running the projections in software like Projection Lab or hiring an hourly planner to run some scenarios for you.

You're lucky to have the 457 because that opens all kinds of possibilities. You didn't tell us your current income, but if you're expecting a $7k/month pension, I would likely continue a high proportion in Roth contributions. Technically Roth 457s aren't available until 59.5, but you could roll the principal over to a Roth IRA and withdraw when you separate.

If you have access to retiree healthcare that might change my answer a bit and you might be more inclined to make pre-tax contributions because you don't have to manage your income for ACA subsidies.

Overall, it seems like you're in great shape!

You and your wife are doing great. This is an optimization question. In an ideal world you would have a crystal ball and know what future tax rates and your future income will be so you can identify which period wild enable to pay the smallest tax.

Regarding future income, if you and your wife inherit someone’s traditional IRA, that could change your future income for a 10-year period because of tax rules on mandatory withdrawals. Something to be mindful of because mandatory withdrawals from an inherited IRA would take up space in your future tax bracket.

Tax diversification is a good thing. Maybe reconsider this “binary” question (Roth vs traditional) with one that prioritizes building tax diversification (I.e., what proportion of Roth and traditional). If you did a 50-50 split contribution, for example, you’d still get an extra $500 tax savings now and your future self will have more flexibility.

I am now retired, with a pension, and have a sizable split of Roth and traditional. I love the flexibility this split provides.

Keep up the good work. Leslie

I'm probably in a similar situation that you will be in, albeit once you are 55. I have a military pension that pays out ~$96K annually. I have a traditional TSP account (similar to a traditional IRA) that has accumulated to over $700K, and will probably be near $900K or more by the time I start my drawdown at 59 ½. My challenge, and I suspect will be yours, is having so much in a traditional account tied with pension income really pushes you up to the 22% or higher tax brackets. Not a bad position to be in, but not really optimized. If taxes end up going up (and they probably will) your traditional retirement savings may be at a higher risk for higher taxes later in life. If you put that money in ROTH, then that it something you will not have to worry about. Plus, ROTH money is not taxed to your heirs if you have a premature departure from this planet. Just my two cents, you guys are on the right track, good on you.

Thanks for all the feedback everyone!! I have been mulling this over in my mind around this for a while since I posted it. Here is what I've come to as a new plan.

1. Change my wife's 401k contributions back to traditional. This will save us some on taxes and continue to build her 401k and have some tax advantage. 2. Capture that savings and put it into the Taxable brokerage account. 3. Keep my current allocations to my 457: Roth, $300 a month. 4. Only max out my wife's Roth IRA for now (don't contribute to mine) to frontload taxable brokerage. This frontloading will hopefully help make my ten year goals more accessible. 5. 3-5 years down the line: increase my Roth 457 contributions to at least the amount that would make for maxing out my Roth IRA. My thought is that I have the 20k in my emergency fund, a large taxable brokerage, and the contributions that are going into my wife's Roth IRA all as "worst case" draws. This means loading my 457 instead of my RIRA makes for earlier accessibility (end of service, not 59.5).

Thoughts on this revised plan?

I am also debating this but from the other side. I have $85,000 into a 401k and $85,000 into a 457b. This is from maxing out my contributions for 2.5 years which has dropped my taxable income a ton and saved me about $25,000 in taxes for those years.

Now after speaking with some FIRE people I'm considering switching to Roth contributions to pay the taxes now and not pay them in retirement.

I think this is a tough decision because both are good options - save on taxes now to accelerate savings and growth… or save on taxes later to avoid RMDs and being able to take out the money I need to live on tax free.

For me it's like I've already done the one so now it's time to consider a switch to the other strategy.

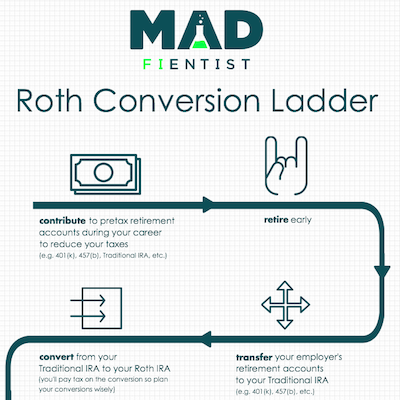

I think a lot of this depends on what age you plan to retire. Like if you are planning to at 45, RMDs arent until age 75, so you would have 30 years to do the roth conversion ladder to deplete your traditional 401k (or IRA) funds. you would still need 5 years of either roth IRA contributions or brokerage account funds to live on while your conversion seasons for 5 years, but as long as you can have that amount by the time you retire I would continue just maxing out pre-tax accounts. At least as long as your tax rate now is higher than you would expect your tax rate to be in the future

The conventional wisdom of "all Roth, all the time" has started to shift within the FI world. IMHO that's a good thing. However, the basis for that shift is the premise "you will be able to withdraw a meaningful amount of money at 0% each year, potentially enough to cover your entire yearly spend, and then a substantial amount more at 10%-12%". But your case is different. If you truly end up with a $7k/month pension (it isn't clear if you are expressing that in 2026 dollars or 2043 dollars but I don't think that makes a tremendous difference), then it is a virtual certainty that you will eat up the entire standard deduction, plus all of the 10% and most of the 12% bracket with just your pension (using 2026 rates and numbers).

Personally, if I were in your boat, I would assume that my traditional withdrawals would be at 22% or higher and then I would look at my current tax rate and decide based on that. Given the size of the pension, I would tend to favor Roth contributions, because once you are no longer employed if you can roll all of that into a Roth IRA then that makes for the nicest/most flexible inheritance vehicle (assuming that you will end up with substantial savings at your passing because of how fat your pension is).

Nice. Thank you. The pension is in 2026 dollars

My thought was that, in the years between age 53 and 59.5, we could draw off of the 457 traditional portion because we would only hand my pension income, assuming my wife retired then too. So one income at 84,000 for married filing joint. Then after age 59.5 start attacking my wife’s 401k traditional portion.

Not to mention, if I save $1000 a year on taxes by switching 457 contributions to traditional, I could add that money to the taxable brokerage account.

Something else to keep in mind is the rule of 55. In the event that your wife still finds herself working at age 55, this rule could kick in and help you out. Basically,if you separate from employment between age 55 and 59.5, you can start your normal, penalty-withdrawals from the 401(k) associated with that employer. If I understand the rule correctly, any balances that were rolled into that particular 401(k) are fair game, but any IRA or 401(k) from another employer are still under the normal 59.5 age rule.

I did not know that! Will look into it. Thanks!

Here is a ChooseFI episode from a few years ago, dealing exclusively with the Rule of 55:

Ep 201 | The Rule Of 55

The IRS allows Rule of 55 distributions but companies aren't required to support it. Reach out to your HR department or look on their webpages for the "Summary Plan Description" for your workplace retirement savings plan. This is a document required by ERISA and is written in plain language rather than legalese. It will say in there somewhere whether or not it supports Rule of 55. My company's SPD doesn't explicitly mention "rule of 55" but talks about distributions after age 55.

Any idea if there are guidelines around that? Could I at age 56 join a company, work there for a month, roll everything into their 401k, and then "retire" and get access to all my previous savings?

The resource guide, under "Tax on early distributions" lists as an exception

That makes me think that there isn't a requirement that employment begins prior to age 55. So, that would appear to make the limitations a function of the ability to roll prior 401(k) assets into the new 401(k) and the vesting period with the new employer.

Link:

401k Resource Guide Plan Sponsors General Distribution Rules | Internal Revenue Service