FIRE in a country with wealth tax

Hello everyone,

Hello everyone,

I would like some insight and advice on the following issue:

I currently live in a country that has wealth tax and plan to FIRE in the next 5/6 years.

What are your thoughts on having to support that significant tax burden while being FIRE?

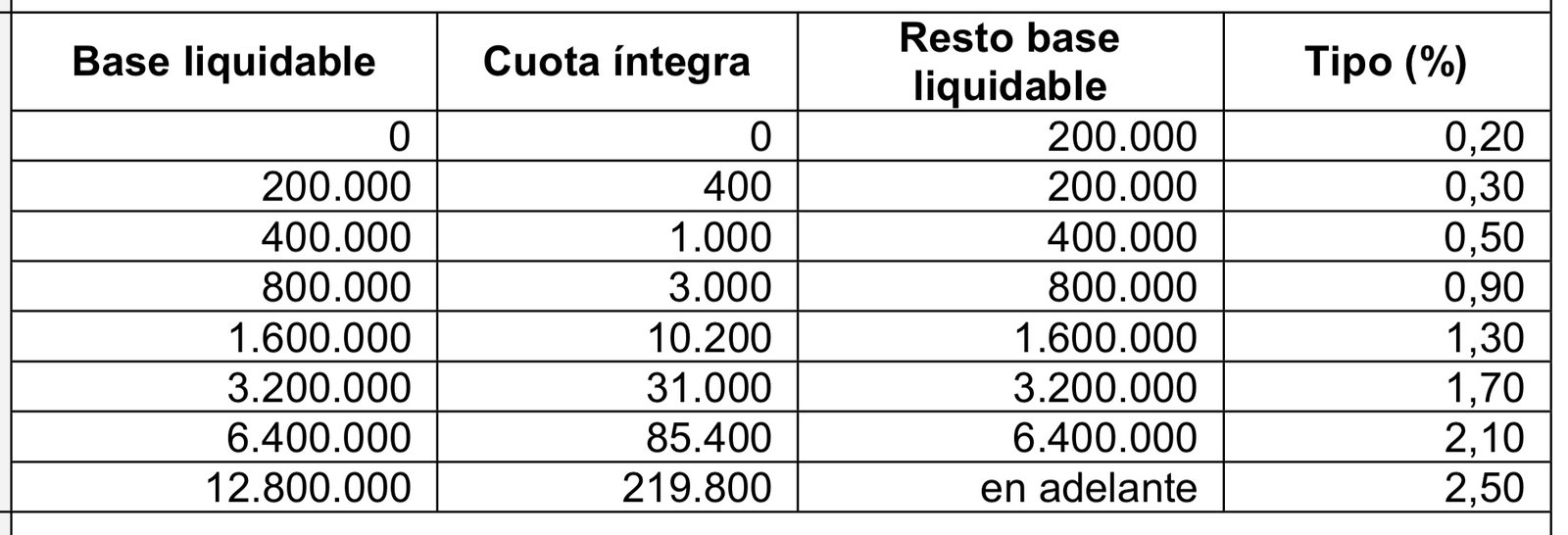

For context I am attaching a screen shot of the current tax brackets for wealth tax.

That is on top of the capital gain tax associated with selling shares on a yearly basis to cover living expenses, and of course shares sold every year to cover the payment of wealth tax.

The options are:

-stay put and sorry for the expression but “bend over” and accept the tax which totally feels like a punishment for having worked, sacrificed, saved and invested

-leave to another country which entails uprooting the family with a child that will be around 10 at the time and finding a place where my partner will have to start her health business back from scratch after 15 years of being established in the town where she currently practices.

We love our place, our ocean view home, our safe town, our child’s school, our proximity to our families, our lifestyle which is by no means expensive where we live… except for that tax! Everything is pretty much perfect… except for that punishment.

Tough decision that has been keeping me up at night for the past several months.

To read the chart: say you have a 5 000 000 net worth; you would pay 31 000, that covers up to 3 200 000 and 1.7% on the difference so (5 000 000 - 3 200 000)x0.017=30 600

So in total for 5M NW the wealth tax is 31 000 + 30 600=61 600

There is a fiscal shield that says you can’t be taxed at more than 65% of your income but you also can’t reduce wealth tax by more than 80%.

I am not going to get into complicated calculations, but it is possible to somewhat reduce the tax, playing with your income but with with higher NW (10M+) it get very complicated and you can effectively be taxed at over 65% on your capital gain cumulating capital gain tax and wealth tax.

In the end it is a very vicious punitive system.

Thoughts, ideas?

Thank you!

Hello everyone,

I would like some insight and advice on the following issue:

I currently live in a country that has wealth tax and plan to FIRE in the next 5/6 years.

What are your thoughts on having to support that significant tax burden while being FIRE?

For context I am attaching a screen shot of the current tax brackets for wealth tax.

That is on top of the capital gain tax associated with selling shares on a yearly basis to cover living expenses, and of course shares sold every year to cover the payment of wealth tax.

The options are:

-stay put and sorry for the expression but “bend over” and accept the tax which totally feels like a punishment for having worked, sacrificed, saved and invested

-leave to another country which entails uprooting the family with a child that will be around 10 at the time and finding a place where my partner will have to start her health business back from scratch after 15 years of being established in the town where she currently practices.

We love our place, our ocean view home, our safe town, our child’s school, our proximity to our families, our lifestyle which is by no means expensive where we live… except for that tax! Everything is pretty much perfect… except for that punishment.

Tough decision that has been keeping me up at night for the past several months.

To read the chart: say you have a 5 000 000 net worth; you would pay 31 000, that covers up to 3 200 000 and 1.7% on the difference so (5 000 000 - 3 200 000)x0.017=30 600

So in total for 5M NW the wealth tax is 31 000 + 30 600=61 600

There is a fiscal shield that says you can’t be taxed at more than 65% of your income but you also can’t reduce wealth tax by more than 80%.

I am not going to get into complicated calculations, but it is possible to somewhat reduce the tax, playing with your income but with with higher NW (10M+) it get very complicated and you can effectively be taxed at over 65% on your capital gain cumulating capital gain tax and wealth tax.

In the end it is a very vicious punitive system.

Thoughts, ideas?

Thank you!

Join the conversation

Sign up to reply, follow discussions, and connect with the ChooseFI community.

Comments

Wow, that's a real shame. I agree that it seems rather punitive.

Identifying the country as Spain is helpful, as it it puts the values into context. For instance, 5M Euros is rather quite different from 5M Mexican Pesos.

That said, it really comes down to what you value, and what level of lifestyle/spending you want in retirement. Up to 1,6M you have a tax of 10,2k. That is certainly not zero, but it also is manageable. Especially so if you really value the things that you mentioned. About a year and half a ago I spent several weeks traveling through the north (Santiago de Compostela to San Sebastián) and I was struck with how affordable things seemed. That said, I wasn't renting an apartment long term or purchasing a house, so I'm sure my perspective is affected by that. You also specifically mentioned a NW of 5M, which has a substantially higher tax burden attached to it.

If I understand the terminology on the chart you provided, this appears to apply to liquid assets only. I'm guessing that means things like stocks, mutual funds, and similar investments, but not things like a home. So, if you own a home without debt against it, that should reduce the net worth that you need to achieve to support your desired lifestyle.

Unfortunately, I am not able to help with things like SWR (i.e., would a 4% rate be sustainable for your particular portfolio), but I can encourage you to consider trying to quantify the value of the things you like about where you are. If you really are targeting a NW of 5M, then you have to ask yourself if the benefits of staying where you are worth about 5,000 euro/month or whether you'd rather trade off the uncertainty and disruption of moving to a new country to avoid that expense.

Thank you. It’s for all assets including real estate, stocks, bonds, crypto, gold, art… everything!

Wow. That's quite sweeping. That probably makes things more difficult, since if you have a home valued at 1M Euros, for example, and that is a substantial portion of your net worth, then you are required to liquidate assets (or obtain income) from a lesser portion of the portfolio to pay the tax on the whole value. But it does make me wonder if they consider all of those things as "liquidable" what is excluded or considered "iliquidable".

The main home gets a 300k exemption.

If lifestyle is "by no means expensive" have you run the numbers to see if you have enough money to not run out of money? It's hard to imagine uprooting a life I love over a tax I could afford.

If inflation in Spain was 1.5% higher than other places in Europe would you have a similar perspective?

I would seriously consider:

a) ways to optimize tax burden. Once you reach FIRE your income could be 0 euro so you would be shielded from most of wealth tax right? But even half way to FIRE amount you might find that tax is big, would that be good time to artificially decrease income? E.g. one of parents not working, your partner might keep all the income in her practice. Also what if you started a company that would own the assets, would wealth tax apply to you? Be creative in how you setup all variable that come to the calculation - income, assets held. b) relocating. As you expect to reach FIRE in 5 years, and then your kid will be 10, this might be right time reconsider location. Would not Portugal be better option from tax point of view? Climate is similar, distance to relatives would not be too big!

Thank you for your comment. On the way to fire, the only way to reduce the wealth tax is by lowering my income, which is doable but I am currently liquidating some real estate and also have some investments that are coming to maturity with the next year so; it’s like I am trying to earn less but I can’t. What a problem. Right 🤣. Yes Portugal is looking like our best option so far. Also once I reach fire, income will not be 0. It will be whatever capital gain is, but I would never be able to escape at least 20% of the wealth tax. Which would mean taking out more money to cover wealth tax and paying more capital gain tax.

To be brutally honest, I think with such an oppressive tax system, I would consider moving to another country as soon I I decide to pursue the path to FI, not after reaching FI. (Consider also how much of "exit tax" you will need to pay.)

Having to pay an annual wealth tax as some % of your portfolio, no matter if you have gains or losses that year, effectively raises the 4% rule of thumb for you to something like 6% or more. Maybe even worse, because on the years with losses, you lose even more (the "sequence of return risk"). It actually shifts the distribution of the expected annual returns, so someone would need to redo the "trinity study" experiment with this tax included. It might turn out that reaching FI in these conditions with an acceptable success rate is not even possible unless you have much more money than needed for the classical SWR = 4%.

I would just adapt your plan to include this tax. A tax that you pay is just a part of your total expenses.

I would not move away from a great place to live, just for this.

I would seriously consider relocating to have a different tax residency and more favorable treatment. The added benefit is that your money can go even further in more affordable countries.

you get the benefit of tax savings and your money going further. You will have enough wealth to still fly home to Spain and enjoy life there part of the year as a non tax resident.

I have a friend who has relocated to Paraguay and likes it. You would have to look at different options but they are out there. With a high net worth you can make many moves.

in 2026 this is more and more common . I’m planning an overseas FIRE also.

I would really consider and even pay for legal advice to make a decision. This single decision could have a huge impact on your net worth and what you leave to your family in inheritance. This single move could keep all that money invested and compounding for you family

What country is this?

Spain

I'm seeing region selection as one option, with Madrid/Andalusia offering 100% wealth tax relief. With the 700k relief per individual, they're also saying to hold assets in both partner names to get 1.4M in relief. Then it looks like strategies include owning shares of small/ family businesses. It does look like the solidarity tax kicks in at 3M, which puts a ceiling on nest egg. Personally, it sounds like I'd geoarbitrage to at least the highest wealth tax relief areas. If my FI Number was 3M, or going to grow that big (likely, over the long term), I wouldn't stick around Spain.

Have you checked in with the Spain ChooseFI Local Groups?

Thanks. The 100% relief is not valid anymore as they put in place the solidarity tax for those regions that did have it. All the other options are rather limited in my case: the small business thing has a specific clause that says 50% of the assets need to be for the actual activity and as far as putting money in the other person’s name, I am not married…I’ll try to check with the local group.