Ultra long term investing (60+ years)?

Earlier I mentioned in another discussion that I plan on making investment accounts intended for my infant nieces and nephews, to fund their retirement. It got me thinking what best to invest in. 60 years is a LONG time, do I really want to bet that the USA is still the dominant country that far in the future? I'm thinking of putting it all in VT rather than VTI.

It's the ultimate set it and forget it scenario, because it will probably need to continue after my death and I don't want my heirs to be able to access it until their own retirement. So whatever I pick needs to have good growth for most of a century.

Any thoughts?

Join the conversation

Sign up to reply, follow discussions, and connect with the ChooseFI community.

Comments

Here's what I did for my son:

- Pick a reputable brokerage account. Make sure I am not paying any assets under management fees to the brokerage.

- Buy 100% stocks of broad based index ETFs.

- Figure out a diversification that feels good. I did 25% S&P 500 equivalent, 25% total world excluding US, 25% US small cap value, 25% international small cap value. I follow Paul Merriman, who shows that small cap historically underperformed, then came roaring back over long time horizons.

- Double check that I actually bought the ETFs after I transferred the cash to the brokerage.

- Make sure dividends are reinvested.

- Turn off all account notifications and messages.

- Forget the password.

- Write a letter to the child that this account exists.

- Set a calendar invite on their 18th birthday to remind yourself that there may be work to do on this account.

- Create a plan to ensure the money goes for the intended purpose in case you're not around.

I created the brokerage account in my name because I don't want him to have to manage or report on this savings until we can get it into a Roth IRA. I'll work with him to transfer it as he gets earned income.

I really mean forget the password. In my mind, this isn't my money. It doesn't matter how much it goes up or down ever. We'll wake up surprised one day.

The only time I need to access the account is for tax reporting each year. I reset the password when I get ready to do my taxes, access the account through TurboTax's brokerage connection feature, and don't dive into any of the information.

This is a super interesting question!

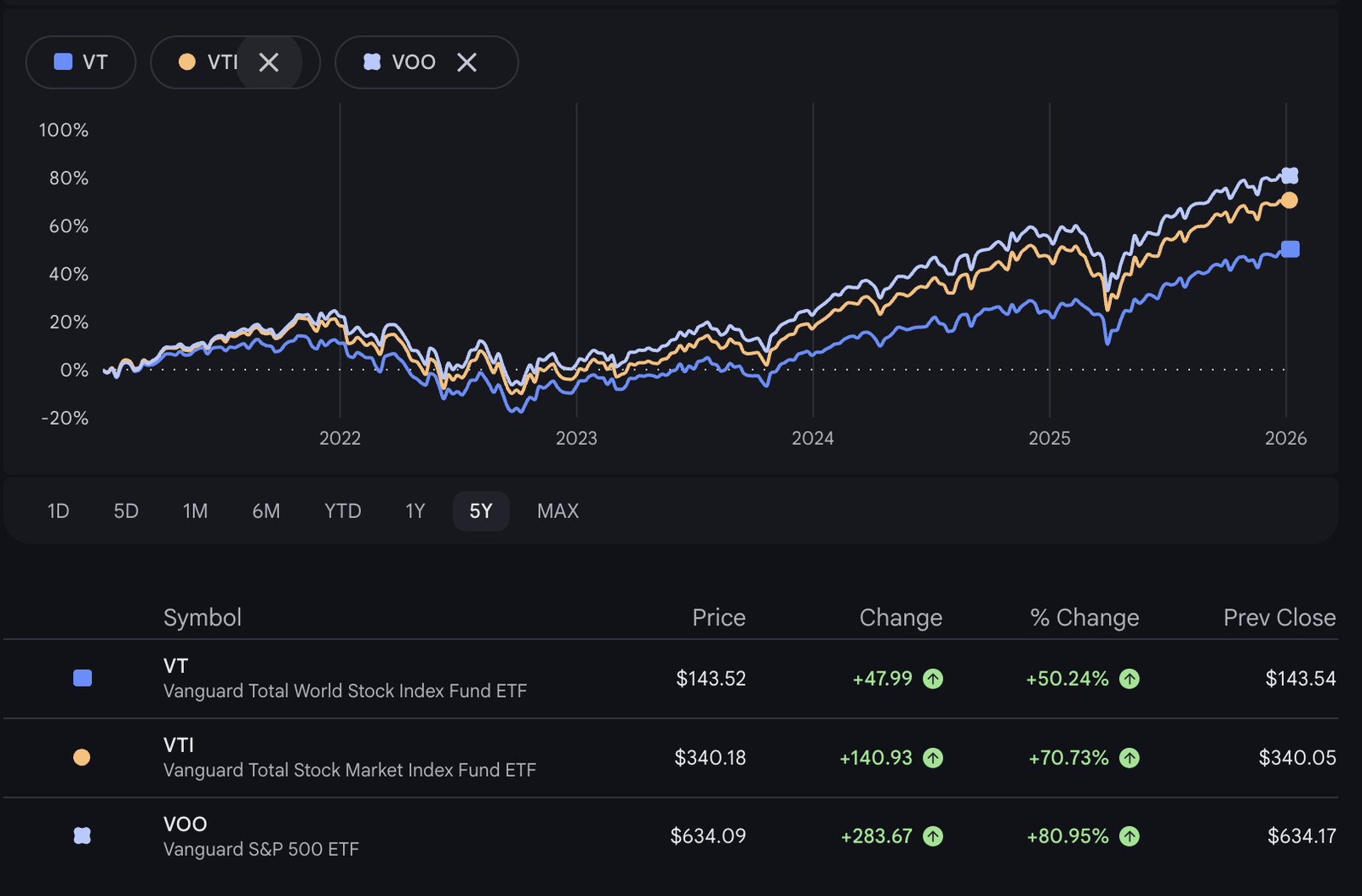

I was curious how VT vs VTI vs VOO performed over the long term. First of all, none of these ETFs are super old so data is limited, I used 5 years since they were all trading at that time. The total 5 year returns for VT were 50.24% (10.04% annual), VTI 70.73% (14.15% annual), and VOO at 80.95% (16.19% annual).

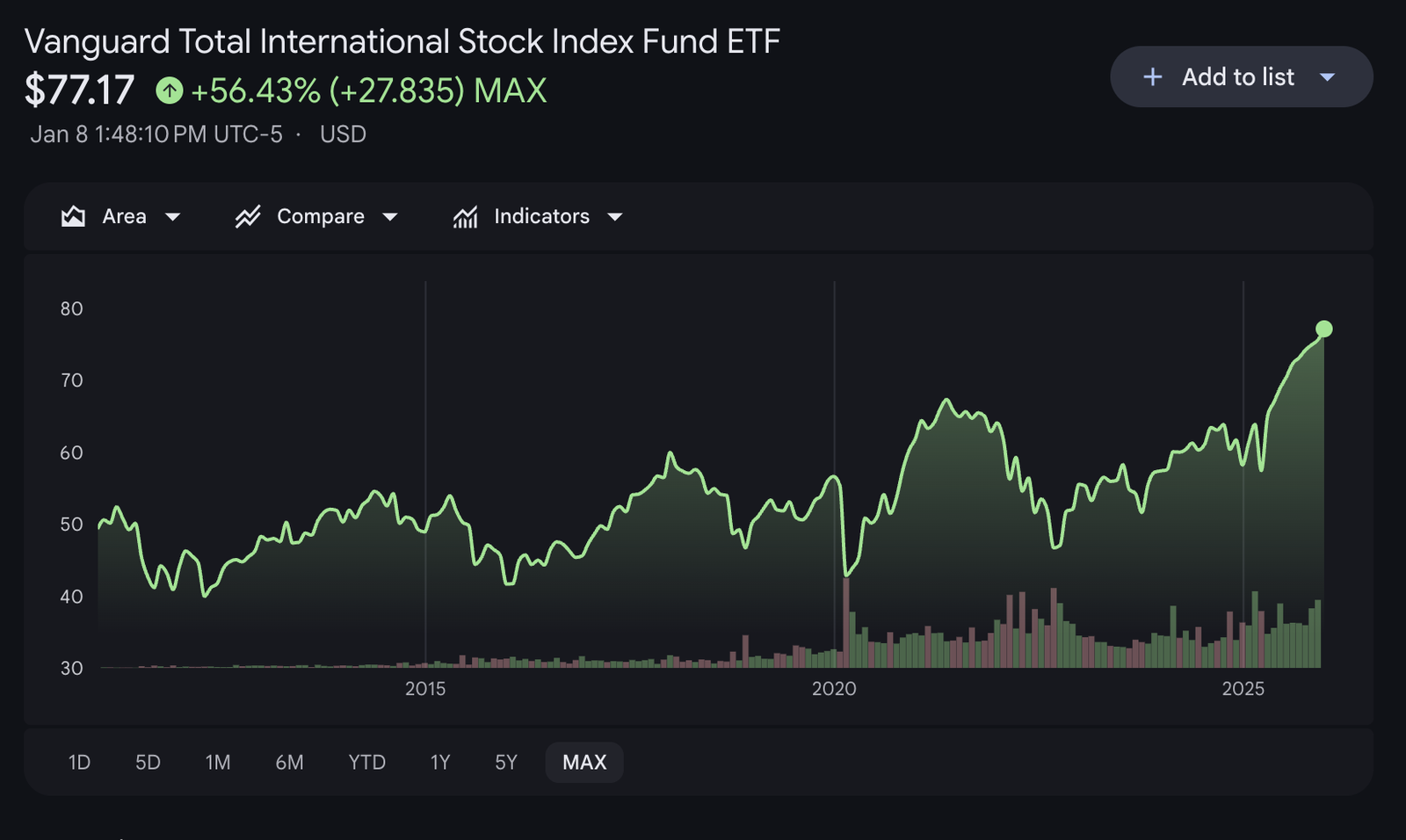

If you look back at VXUS which has been trading since 1/28/2011 the total return is 56.43% or 3.762% annualized. I used VXUS to strip out the US represented portions of VOO and VTI.

Obviously, the US stocks are responsible for the lions share of returns in VT.

The expense ratios for VOO and VTI are 0.03%, and while still small; VT is double at 0.06%

It would also be interesting to see the international influence on VTI and VOO which I believe is significant and represents the best of the international markets; think NVDA, AAPL, MSFT, AVGO, LLY, CVX, etc.

I have little international exposure and no VT or VXUS in my portfolio. I am mostly invested in VOO for the index portion of my portfolio. In thinking about this post, I think country specific ETFs might offer some of the best growth while eliminating some drag of the worst preforming markets but that would necessitate further research.

The question is, though, will the US still be the dominant market force in 50 years? I don't think we can say. The data I really need is whether a world fund is "good enough", or if I should take a more active role in the investments while I'm able to (ie invest primarily in US stocks now, and if global circumstances change in 20 or 30 years I can rebalance).

Of course, no one knows who the global economic power will be in 2076. Did we know where the world would be 50 years later in 1976? Not really, it probably wouldn't have been a bad assumption that the US would still be a global super power. Currently the US represents approximately 50% of the world markets and we have obviously dominated the world economic stage in the past 50 years.

If "good enough" is your ultimate question; the answer could only provided by you; as you know your risk tolerance, your knowledge or lack of the global markets sans the US market, and how you see the future of the would markets. Are you willing to accept less returns (historically) for broader diversification? Are you willing to accept broader diversification in exchange for potentially higher total returns (future looking)? Knowing the information from my post above about past returns as well as evaluating on a frequent basis is probably the best answer. Did the world markets do well last year? Yeah, 32.3% is outstanding by anyones metrics; did it beat VTI (17.1%) in 2025; yeah, by a good amount. Will this continue to be the case? Who knows, if the past is any indication of the future, probably not.

Personally, I evaluate my holdings twice a year. This helps me rebalance as well as gives me an opportunity to see if my holdings still reflect my investing philosophy. Something that always sticks with me is Brad saying "Strong opinions, loosely held". For me, adding any significant international exposure is something I will continue to evaluate.

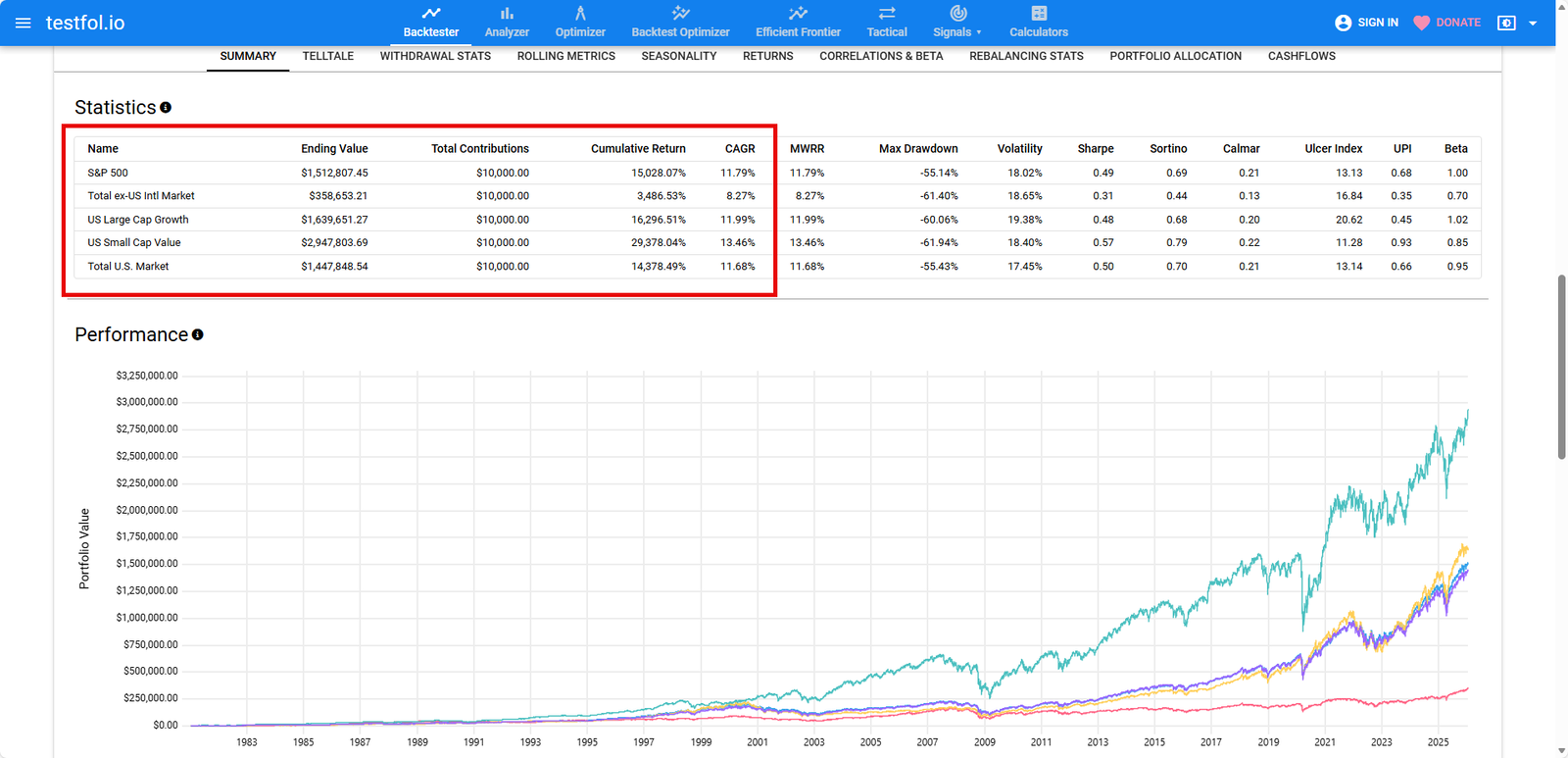

I would agree with what Craig shows and appreciated other's conversation around this. For backtesting, while you can't use the specific ETFs, use the asset class. Here is a https://testfol.io/?s=4IrmUOpG5Yz analysis going back to 1981 that shows that Small Cap Value is the clear winner (even more so if you go back into the 70s). But as none of us have a crystal ball that works, I would lean towards 50% large cap growth and 50% small cap value with some mix of international and check in every few years.

In my account for my kids, I also added 5% Bitcoin five years ago and will just see where that goes.

One other item on what you mentioned, why not allow them to access the money earlier then retirement? What if they need that money earlier due to health issues or retire early? Agree don't want them to have it when they're 20 but may be better for them to have access to at least some of it when they most need it.

![]

Honestly? I don't trust em. Not when they're 20, not when they're 40. Most of my family is abysmal with financial education, especially that branch. They're very traditional Southern "get married young, have a ton of children, husband works while mom stays home" families. I imagine their kids will get very poor financial education.

And if it turns out they actually do take an interest in personal finance, they can effectively "use" the money by reducing their own retirement savings. I'm thinking of setting something up at like age 30 so the kids can view the money but not take control of it, ideally. That way they can plan.

I just don't want them to be like so many millenials saying "my retirement plan is to work until I'm dead". I believe in this country we should have more robust pensions and social security and healthcare so people don't have to do the kind of planning we do, because most people can't or won't plan like we do. I can't provide that for the entire country but I can do it for some people.

When you say you don't want your heirs to be able to access the funds until their own retirement, what's the legal structure to put that into place? A trust with practically zero flexibility could be challenged in court, however I am not an estate attorney and this is definitely estate planning stuff.

As to the investment question, who knows. The US does not have to remain "the" dominant country in the world to be a great investment. It helps, but it's not required. VT is the simplest global fund solution today. But will VT exist in 60 years? SPY is the oldest ETF at 32 years old.

I like the idea of being globally diversified. I personally chose an India ETF as one holding in our kid's accounts, partly to express that ultra long-term view. But like all plans, monitoring is required.

I have no idea what the legal structure would be. I'm assuming some sort of trust, but I'd need a lot of research and I'd need to consult with an estate attorney.

I would purchase VT. Who knows what the world will look like in 60 years.