Question on asset "location"

Hello, seeking some clarification on the discussion regarding asset location. I follow that it is more tax efficient to have equities in after-tax accounts and have bonds or other interest-earning investments in tax-advantaged accounts. Does this only matter when in drawing from all account types (after-tax and tax-advantaged accounts)? It definitely makes sense for the 60 year old person who withdraws from every type of account as desired. But what about a 40 year old FIRE'd person who doesn't plan to tap the pre-tax accounts for 20 years (presuming enough in other accounts to bridge the gap)?

My general thought is that money earmarked for not being touched for 20 years is better off in equities and seeking more growth than some bond mixture. If only after-tax accounts are earmarked for those 20 years, then "asset location" is not important for a good duration of time (e.g., 15 years) and the focus would be on "asset allocation" for the after-tax account portion.

Join the conversation

Sign up to reply, follow discussions, and connect with the ChooseFI community.

Comments

If you don’t already, You may want to research risk parity radio to learn more about retirement portfolios. Check out this introduction.

The Secret to a 5% Safe Withdrawal Rate | Frank Vasquez

On his podcast page you can search for topics as he’s talked about this realm many times. Riskparityradio.com

The problem with bonds (and REITs) in taxable accounts is they throw off ordinary income, which you are then forced to pay taxes on at a high marginal rate even if you don’t need the money, vs equities that throw off a smaller amount of qualified dividends and then capital gains when you sell, both of which are taxed at a lower rate—possibly 0%. The latter is obviously much better for your total after-tax return.

The issue with the “asset swap plan” so far as I can tell is that you may well run short on assets to sell in the taxable accounts if there is a bad sequence of returns. It works well right up until the things you’re selling/buying (typically equities) fall significantly in value and you run the after-tax well dry (or lean on it hard enough that you’re worried it might run dry, which would be stressful). I see asset swaps as a useful tool but would give sequence risk some thought unless you’re good with diving into 72t withdrawals to supplement if things go poorly.

If the taxable well runs dry unexpectedly, look at 72t or just eat the 10% EW penalty, depending on how many years are left until 59.5. If you think this is likely, however, leave enough in a work 401k to at least take advantage of the Rule of 55.

The asset swap approach is great, but this is my concern with this approach as well - you can run into liquidity issues if equities are down while selling them in your taxable account to fund your life. It's part of why I'm waiting until the year I turn 55 so I have another source I can access that does include more than just equities.

If you're 5+ years away from FI, you shouldn't be holding any bonds in the first place. 50% VTI (or equivalent) and 50% AVUV, rebalance once a year, and done.

- Totally agree, bonds are terrible when governments debase the future of money so much.

- My only tweak is no bonds regardless of time frame until bonds make sense, which they have not in a while, and do not …right now.

- Investments into stores of value and businesses only, avoid credit.

- Bonds will be good when inflation normalizes 0-2% or deflation happens, neither is likely anytime soon.

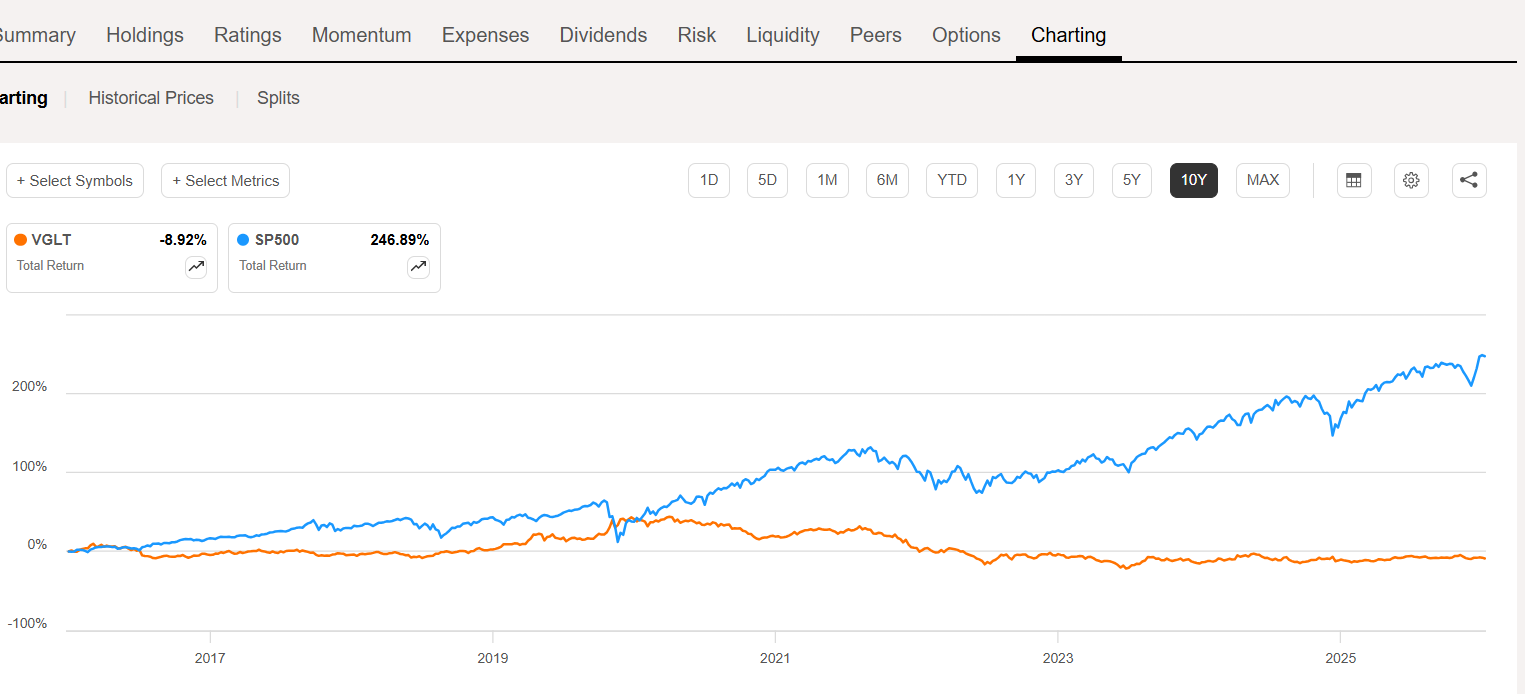

Bonds have a bad rap these days, but that is mostly due to Vanguard/Bogleheads pushing total bond funds (BND), which hold mostly low-return, highly-correlated garbage. Long-term treasuries (VGLT) specifically are an essential part of a drawdown portfolio.

Replacing BND with VGLT makes a portfolio more aggressive. It can provide better protection during a stock market crash, but it will suffer much deeper losses if inflation stays high or interest rates continue to climb. For someone in or near a drawdown phase, VGLT is often used in a smaller sleeve rather than as a total replacement for intermediate bonds to avoid over-exposure to interest rate swings.

You can hold VGIT and VGSH too if you want for different term risks; the most important thing is ditching the VCLT, VCIT and VCSH garbage inside BND. Personally, my bonds are 100% GOVZ (treasury strips) to minimize how much space they take in my portfolio so I can allocate more to other asset classes.

VGLT performance total return: 1 yr, 3 yr, 5 yr 10 yr VGLT is definitely contributing to a drawdown portfolio 🤣 but not in the way investors may want. There was a few in 2020 days when they had a similar return, so I guess if you are timing the market and are VERY patient and well informed and emotionally stable… (ie: not human) maybe?

VGLT performance total return: 1 yr, 3 yr, 5 yr 10 yr VGLT is definitely contributing to a drawdown portfolio 🤣 but not in the way investors may want. There was a few in 2020 days when they had a similar return, so I guess if you are timing the market and are VERY patient and well informed and emotionally stable… (ie: not human) maybe?

Asset allocation in a drawdown portfolio is not about total return; it's about improving the safe withdrawal rate by diversifying into uncorrelated asset classes.

Thanks for asking this question! I've been wondering the same thing! I've been listening to Risk Parity Radio (currently on episode 84) but it hasn't addressed this specific question. If you can't access those tax-advantaged accounts for 20 years (or even 5 if you plan to do Roth conversions), how do you access the bonds/gold if there is a downturn in the stock market? I understand an asset swap, but wouldn't you have to sell stocks at a 'low' to swap out for the gold/bonds that you sold off?

So this part I'm clear on regarding an asset swap (after an allocation is decided upon). After-tax account holds Stock A, and pre-tax account holds stocks/bonds/gold. Stocks are down and you want to sell some bonds/gold for your living expenses. The process is to sell $X of Stock A for living expenses from the after-tax account, and then exchange $X of bonds/gold for Stock A in the pre-tax accounts.

You get money for daily expenses and your allocation should still be in place after transactions. Idea being selling Stock A in your after-tax account has minimal taxes as a bonus.

The entire idea of the asset swap is that you simultaneously sell it low in one account and buy it low in the other account, which effectively moves the asset from one account to the other with no net change in the portfolio. Just take care to avoid wash sales if you realize a loss in the taxable account.

Yeah, I put my S&P 500 ETF for mutual fund in my work 401(k), with no bond allocation because I have 20 years of projected growth at me. However, for my more aggressive and speculative “ QQQM.” I put in my Roth because I want all those dollars to be tax-free. Also I buy my spec bucket is in my after tax brokerage to allow for tax loss harvesting and tax gain harvesting.

However, if you were closer to retirement, it would betresponsible to de-risk and have a bond allocation

, and I would put that portion ideally in a work 401(k) or tradittonal IRA, so if you do get taxed you’re getting taxed on the Least productive dollars.

Asset allocation (AA) is the first consideration. Where to locate assets is a secondary consideration.

Let's say retirement is 20 years away and you have a high risk tolerance. You opt for an AA of 100% equities. You're trying to save as much as you can so you max your Roth IRA, pre-tax 401k and put additional savings into a taxable account. If your AA is 100% equities, each of these accounts will contain all equities.

But now let's say retirement is 20 years away and you have a low risk tolerance. In addition to equities for growth, you want to hold treasuries and managed futures to smooth the ride over the next 20 years. You continue to hold only equities in the Roth IRA to take advantage of the tax shelter on those growing assets and you continue to hold only equities in the taxable account for the favorable LTCG tax rate on gains and qualified dividends. You hold the treasuries and managed futures in the pre-tax 401k to defer tax on the ordinary income those throw off.

But you have a lot more money in the pre-tax 401k than your AA percentages for treasuries and managed futures, so the remaining portion of the pre-tax 401k will also contain equities.

So it isn't that you're drawing on the accounts or not. You start with your AA and then locate assets for tax efficiency.

I appreciate the reply. I interested in the situation where someone is retired at 40 and has the after-tax funds to cover the 20 years until accessing tax-advantaged accounts at 60. Does asset location even factor in this situation?

I think I see your question. You’re asking about what is called a bucket strategy. The advice goes that you should hold money for different time periods in different buckets (or accounts) and those buckets should be invested according to when that money will be spent. So our 40yo would have one bucket (“after-tax funds”) for now until 59.5 and a second bucket (a retirement account) for years 59.5+. Because the retirement bucket won’t be tapped until 20 years from now, it should hold all high-growth assets (equities) and no low-growth assets (bonds).

Unfortunately this isn’t a great way to think about your accounts. The bucket strategy would have our 40yo holding tax-inefficient bonds in their taxable account simply because withdrawals will come from that account first.

You should think of all your accounts together as one single portfolio. Equities grow your overall portfolio and bonds reduce volatility in your overall portfolio regardless of what account they’re located in. So you should instead choose asset location according to its most tax efficient placement.

Why Boston said. Check out risk parity radio, has had a lot of episodes answering this question in detail.

Ok, so if my understanding is correct, the bucket strategy has big drawbacks. Better to do a whole portfolio plan and tap the tax-advantaged accounts at 40 via the various methods.

In that scenario, the tax-advantaged accounts would hold some desired portion of bonds and the after-tax accounts would be tilted towards equities for tax reasons (e.g., a decent cash account and equities in after-tax, and some allocation of equities and bonds in the tax-advantaged accounts).

tldr: "asset location" ideas and the bucket strategy don't go well together.

Relatively correct. Learn about asset swap. It’s when in retirement you sell equities in your brokerage to live off of, but then sell bonds in Ira and buy stocks. Especially as being so early you can have up to 30k of income and 90k of capital gains and pay no federal tax.

Specifics, details, location matter but if you’re in this type of scenario you have done great and worth finding an hourly fee only advice only advisor to help walk you through the details.

There are ways to access retirement accounts before age 59.5 (72t, Roth conversion ladder) but they're on the rigid side and require careful planning. In our scenario, our 40yo has 20 years of livings expenses in "after-tax funds" (so cash equivalents, taxable account, Roth IRA) so using that first makes sense.

Cody Garrett, CFP®and Sean Mullaney wrote a fantastic book that can help you think through this kind of tax planning: Tax Planning To and Through Early Retirement

.

You want to be mindful of how cash is taxed, especially if you're building up a larger position in cash. Cash in a HYSA or cash held in money market funds (MMF) in a taxable account throw off tax-inefficient ordinary dividends/interest every month. There are a couple of ways to hold cash but avoid the continuous flow of ordinary income it throws off.

One strategy is to keep cash in a retirement account so that the ordinary dividends it throws off isn't taxed each year. The way you would access that cash even while you can't yet take distributions from the retirement account is called an asset swap. The gist is you sell something in your taxable account and withdraw that cash. Then you purchase in the retirement account the same thing you just sold in the taxable account. The end result is you've withdrawn cash but your allocations have stayed the same and you're subject only to capital gains tax in the year of sale. Justin from Risk Parity Chronicles has published a nice video walkthrough on how an asset swap is done

.

A second strategy is to hold shares of the BOXX ETF inside your taxable account. BOXX mimics the yield of 1-3 month T-bills so its yield is similar to a HYSA or MMF. The benefit is that because it's an ETF it doesn't throw off interest/ordinary dividends like cash does. When you sell shares, you're taxed on earnings at capital gains tax rates.

Using BOXX takes a little planning to take advantage of LTCG tax on earnings—you would need to hold shares for at least one year. But worst case scenario is that you might sell shares before one year and be subject to STCG tax on earnings. Paying STCG tax on earnings would be no worse than holding cash in a HYSA or MMF and accruing interest/ordinary dividends every month.

Joe mentioned the Risk Parity Radio podcast. That podcast is really the best single resource out there to learn this stuff. I'm a long time listener. Check out episode 190

. If it clicks with you, go back and listen to the foundational episodes which you can find on the RPR website's episode guide.

I don't quite understand this .. I've been trying to align to a risk parity portfolio, but I have much more assets in tax-deferred and Roth accounts. I understand the tax inefficiency, but it seems prudent to align my after tax brokerage in such a way to preserve assets for the next 5 years (and start Roth conversions right away).

I'm still trying to align my profile as one big bucket, but I am trying to align my after tax brokerage with bonds and gold to hedge some risk, because a bad market fall would make SORR painful in that account.

The tax inefficiency doesn't seem like it would really make a huge difference, but maybe I'm looking at all this wrong. Thoughts?

Frank talks about RP portfolios for intermediate-term spending from time to time. Gold doesn't usually do much so you're not selling it frequently. You may go with large-cap value instead of SCV for the value tilt and intermediate treasuries instead of long treasuries—these tweaks lessen volatility. Consider holding cash in BOXX instead of short-term treasuries, a MMF or HYSA or using asset swaps to access cash. Tax loss harvesting will also help with taxes.

Here are 3 episodes to check out.

(The platform isn't letting me insert more than one link otherwise I'd link to the episodes.)